|

Last week we saw one of the key benchmarks completely broken, and if there was any doubt, this is what happened this week. The Frenchs are gone

|

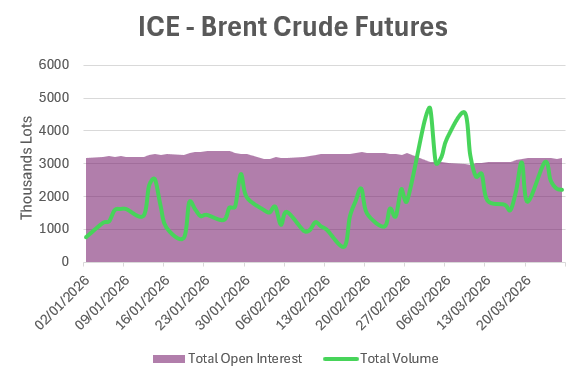

Alright, but at least we still have futures to guide us, right? Well, this week made it clear that manipulation exists and now it’s present in Brent futures as well.

|

In WTI, we already saw it last week, with the spread versus Brent at historical highs (since the export ban was lifted). At first, we thought this was driven by SPR releases weighing on WTI, but the barrels that are about to hit the market are mostly Mars grade, and Mars vs WTI is at $8, near the highs. Midland, the export-grade crude in Houston, better known as “WTI FOB”, is also at WTI +3… nothing suggests these markets are oversupplied, quite the opposite.

|

WTI prices are tied to deliveries into tank farms in Cushing, Oklahoma… and even looking at inventories, there’s no indication we’re anywhere near tank tops so a $13 spread to Brent makes no sense. Either someone really believes exports could be indeed banned, or someone is aggressively selling the front-month… I lean toward the latter.

|

So if we can’t trust swaps, and we can’t trust futures, what is oil, the physical barrel, actually worth? This is becoming a recurring problem, as it’s increasingly difficult to assign value beyond benchmarks.

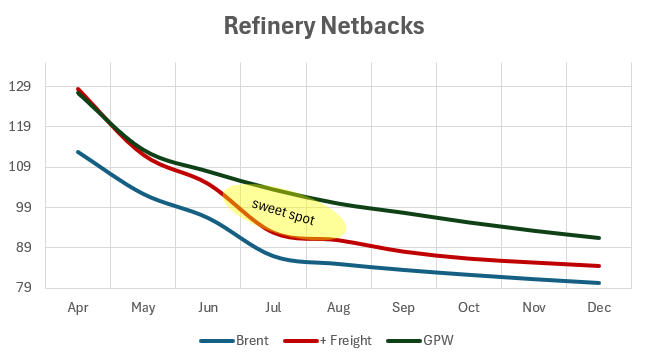

We won’t go into utility value, calorific content, or energy output… in times like these there’s a simpler framework: refinery netbacks. Essentially, you deconstruct the entire supply chain backwards to answer the most important question: how much is a refinery willing to pay for my barrel?

|

To begin with, we need a set of assumptions, mainly understanding the yield of a barrel across different refinery configurations. The industry standard for linear programming is PIMS, used by virtually all refineries to optimize operations from crude selection and run rates, to tweaking outputs for more diesel, more gasoline, domestic specs or export specs, and so on. Decades ago, this was just proprietary to refiners, but as trading has become more sophisticated, this information has filtered downstream, even small oil producers today can estimate full refinery margins by modeling Gross Product Worth (GPW).

GPW: $110.91/bbl

Processing costs: -$6.00/bbl

Refinery margin target: -$4.00/bbl

─────────────────────────────────────────

Refinery Gate Price: $100.91/bbl

Freight or pipe: -$2.50/bbl

─────────────────────────────────────────

Implied FOB Crude Value: $98.41/bbl

Brent Future Price: $94.41/bbl

To calculate GPW, we need prices and the easiest way is to look at product swaps or futures (easy, not correct, but good enough for now).

The price that matters to a crude trader is the Refinery Gate Price, the total feedstock cost delivered. This includes freight (the largest component), but also insurance, financing, in-transit losses, and so on.

Strip those out, and you arrive at an implied FOB value and the difference between that FOB and the front-month futures are our beloved “FOB diffs”… that’s what we should be capturing. Sounds simple, right? Not quite.

Optionality

This is where traders make their money. A crude trader exploits the constraints of smaller producers those without the logistical capacity or the time to run multiple refinery models across destinations. In the Excel example I used Singapore, but it could just as easily be Rotterdam, the USGC, or anywhere in the world, not necessarily a pricing hub. This is where freight becomes critical.

As the chart shows, time, or transit time, also matters. Depending on where you send your barrel, you’re exposed to different forward curves, with different degrees of backwardation, meaning that in some cases you won’t even land above GPW.

But just like we have FOB diffs for crude, refineries have their own cash diffs or spot differentials, typically ranging between -1 and +1 versus the relevant product future, since products are relatively homogeneous. Today, in Asia, gasoil is trading at Singapore 10ppm Gasoil April swap +$30/bbl. And when you have $30 to play with, any crude from anywhere in the world works—as long as you load now and arrive in April.

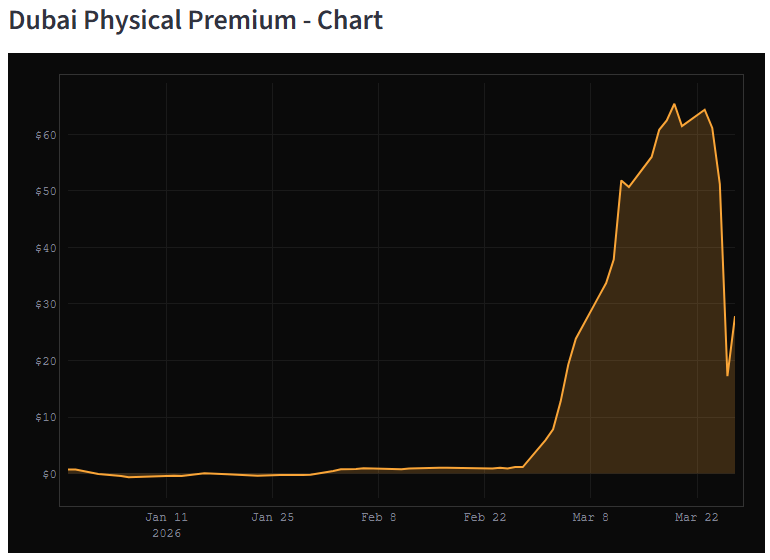

That’s why this week we’re seeing an explosion in crude FOB diffs, with no real correlation to quality specs..everything is trading at Brent +5/8/10 or whatever… it’s a gold rush to load as fast as possible. You see it in freight too, contrary to what I expected a few weeks ago, there are more cargoes than ships in the Atlantic. With spreads this wide, you get absurd flows, like loading an Aframax in Houston to China via the Panama Canal… something that makes no economic sense under normal conditions. As a consequence, the freight market is also broken.

In effect, what we’re trading is Asian gasoil—using crude or freight as proxies—but the real exposure is gasoil in Asia.

Why should I care?

Despite the volumes being loaded today, it’s not near enough to offset the loss of Middle Eastern supply, so the gasoil deficit remains. On top of that, most of what’s heading to Asia (light sweets) are not optimal crudes for maximizing gasoil yields.

That $30 premium is there for April, but there’s no guarantee it will be there going forward. This creates operational challenges for refiners: they can justify buying crude at Brent +10 today, hedging only with Brent futures, because that +10 is essentially unhedgeable exposure. But that’s risk they might not want to take if they only have the gasoil swaps as price guideline for next cycle sales—so they’ll push for FOB diffs to compress back toward benchmarks.

That leaves only two adjustment variables: is either freight or flat price. Is true that right now, ships are capturing most of this inefficiency, if an arb is $20/bbl, they will charge you $20. It now becomes a matter of how the market players redistribute the windfall profits. Big oil might have a say there.

Inevitably, benchmarks will have to move higher. Today, an Asian refiner could practically buy WTI futures on NYMEX, take delivery in Cushing at expiry, move the barrels to the coast (+$2–3/bbl added), and bypass differentials altogether.

|

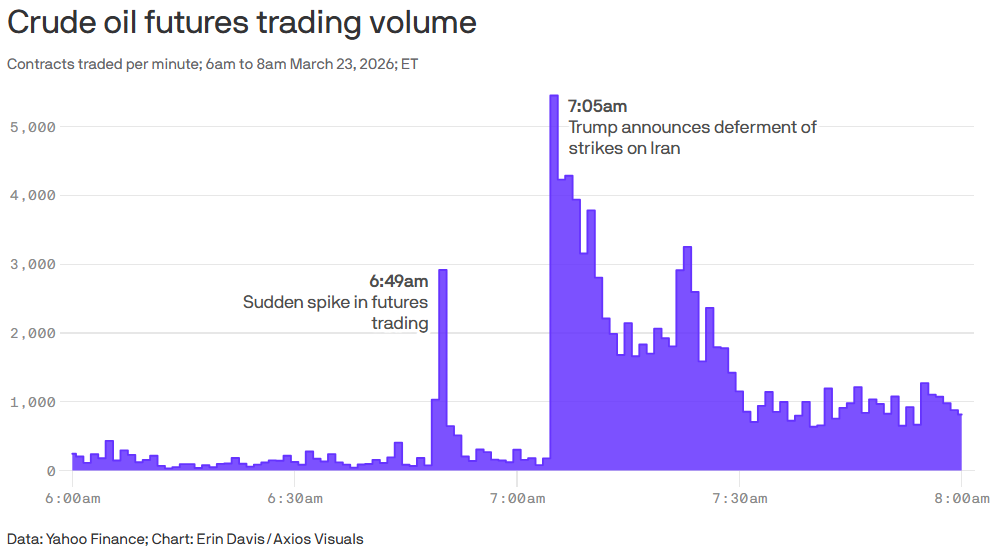

That pressure is already building—which is why we’re seeing $2–3 daily moves regardless of what Trump does. Volatility can be suppressed in the short term, but the direction is already set...

Keep reading with a 7-day free trial

Subscribe to Oil not dead to keep reading this post and get 7 days of free access to the full post archives.

A subscription gets you:

| Oil Weekly Commentary | |

| A custom App and chat | |

| We might start doing webinars |

![]()

![]()