Prediction market microstructure | I write about sports gambling around here more than I used to, because sports gambling has become pretty closely integrated with postmodern financial markets. Sometimes, when I write about sports gambling, I get emails from readers explaining that sportsbooks set their betting lines to balance bets on each side: A sportsbook sets the odds or point spread of a game so that it will pay the same amount of money regardless of which team wins. The book will collect, say, $100 of bets on the favorite and $50 of bets on the underdog, and it will set its odds to pay out $140 if the favorite wins and $140 if the underdog wins, keeping $10 — the “vig” — for itself in either case. This is a popular view of sports betting, but it is wrong. It’s not entirely wrong: Sensible sportsbooks will manage risk and try to keep the action somewhat balanced. But in fact many sportsbooks regularly make directional bets on outcomes: They have some view of the likely result, and they set their odds to, in effect, bet on the more likely outcome. [1] And then sometimes they lose money on a game, and other times they win money on a game, but if their models are good they win more than they lose and are more profitable than they would be if they always balanced bets exactly. Intuitively, the general public is systematically wrong — people tend to irrationally bet on their home teams, underdogs, etc. — and taking the other sides of those bets is generally profitable. The sportsbook might stay “close to home” (not too much risk either way), but it doesn’t have to be “flat” (no risk either way). It is not looking to take no risk; it’s looking to take the right risk. [2] Loosely speaking, the role of bookies in the stock market is played by electronic proprietary trading firms. [3] If a retail investor wants to buy a stock, she will probably buy it from Citadel Securities or Hudson River Trading or Virtu or Jane Street or someone like that. Those trading firms will sell some stock to one retail investor one second, and buy some stock from a different retail investor a second later. You could imagine the trading firms working more like the popular perception of bookies, or more like actual bookies. That is: - Trading firms might buy 100 shares of Stock A one second and sell 100 shares of Stock A the next second. Over a second or two, they might be long or short Stock A. But over the long run, they try very hard to stay “close to home,” and every night they “go home flat,” with no net positions in any stocks. They make money only by capturing bid/ask spreads in short-term trading.

- Trading firms might have some fundamental model of value, and if people want to sell Stock A below its fair value they will keep buying. If a firm accumulates 10,000 shares of Stock A during the course of the day, that’s fine. If it holds those shares overnight, or for days at a time, that’s fine. The point is not to be flat, but to be right. If the trading firm is systematically long stocks that go up and short stocks that go down, then that’s much more profitable than staying flat.

As with actual bookies, the truth is mostly somewhere in between. A lot of proprietary trading firms will have some model view of value, and will try to buy stocks below their value and sell above their value. They will have other constraints — risk limits, capital, etc. — that tend to push them to be close to home. The result will be a trading book that has much less directional risk than, you know, Bill Ackman’s portfolio. If an electronic trading firm had large long positions in 12 stocks and held them for months, that would be odd. But there can be some directional risk: If a trading firm ends each day with zero net position in every stock, it is leaving some money on the table. Things are a bit easier for stock trading firms than they are for sportsbooks, in that financial markets have a lot of correlated instruments that can hedge each other. If a firm is long $100 of Stock A and short $100 of Stock B, that might be less risky than either position on its own: If Stocks A and B are correlated, their moves will mostly offset each other, and the firm is unlikely to lose anything close to the full $200. Or an options trading firm can hedge its options position with the underlying stock — long call options on 100 shares of Stock A, short 60 shares of Stock A to hedge — and won’t make or lose much money whichever way the stock moves. A stock market maker can have a lot of long positions and a lot of short positions and still feel, on balance, close to home. This is harder for a sportsbook: We have talked around here about sportsbook correlation models, but they have limited applicability (same-game parlays); as far as I know it is hard to hedge a bet on the Yankees with a bet on the Mets, or on the Masters for that matter. Financial assets tend to move together based on underlying economic factors; baseball games do not. There is no obvious reason that the result of the Mets game would tell you anything about the result of the Yankees game. [4] Really, there is a range of these electronic proprietary trading firms: Some take very little directional risk and try to go home flat in everything most days; others have more complex hedging models that allow them to take lots of individual risks while keeping overall risk low; others will make unhedged billion-dollar directional bets if the expected value is good enough. [5] Anyway, one reason I write a lot about sports gambling now is because I write a lot about prediction markets, which are sort of legally financial markets (in the US, they are commodity futures markets regulated by the Commodity Futures Trading Commission) but practically sportsbooks (79% of volume on Kalshi is sports bets). One frequently remarked difference between a prediction market and a traditional sportsbook is that, at a sportsbook, customers are betting against the sportsbook, while in a prediction market they are betting against each other. I tend to be unimpressed by that difference, because it is also true of the stock market: Anyone can buy stock, and anyone can sell stock, so when you buy a share of stock you might theoretically be buying it from some other investor who wants to sell. But in practice you are almost certainly buying it from an electronic trading firm, because those are the firms that make markets on the stock exchange (and, more relevantly, for your retail brokerage). They are posting orders to buy and orders to sell, and if you want to sell or buy you will probably trade with their orders. Similarly, in prediction markets, in the long run, it seems entirely plausible that customers will mostly trade with market makers: Professional electronic trading firms will post bids and offers on the prediction markets, and if you want to buy a contract you will in most cases buy from a trading firm that sells it. If the contract you want to buy is “Mets win tonight,” you will buy it from a trading firm that is in effect betting on the Mets losing. And then if someone else wants to buy “Mets lose,” they will also buy it from that trading firm, which will be trading on both sides of the market. But: - We’re not there yet: There are some professional prediction-market traders who provide liquidity, but they do not yet seem to dominate volumes on the big prediction markets.

- Who will these market makers be? There are some reasons to think that they will be the same prop trading firms that trade stocks and options and futures: Those firms are good at trading regulated financial assets, and prediction markets are regulated financial assets. But there are also some reasons to think that they will be the same sports market makers that make odds for sportsbooks: Those firms are good at trading sports bets, and prediction markets are sports bets. (Of course there is overlap; Susquehanna famously does both.)

- If the market makers are traditional prop trading firms, they will have some difficulties an adapting to prediction markets, because the traditional correlation and hedging math of financial markets might not work as well in sports or other events.

So Bloomberg’s Bernard Goyder reports on prediction markets: There are numerous reasons why institutional traders have not joined in, including the lack of regulatory clarity and the relatively light volumes compared with the other areas where they operate. But a new academic paper points to another potential reason: Some of the basic tools that sophisticated traders use to manage risk in other markets aren’t available in event-based bets. At the most basic level, most market makers offset their risk in one type of trading by hedging with other related assets — for options markets, they can do this in the underlying stock market. That is much less easy when the bet is on a celebrity wedding or an election, according to the paper published by Nick Palumbo, a former product manager at the sports betting site DraftKings Inc. Here is Palumbo’s paper, “A Microstructure Perspective on Prediction Markets,” finding that market makers on prediction markets don’t really earn bid/ask spreads so much as they make directional bets on events: Passive liquidity providers systematically absorb residual demand imbalances and retain outcome-dependent exposure through contract resolution. Profitability appears to depend less on classical bid-ask spread capture and more on managing terminal risk associated with dynamic supply creation. These findings suggest that liquidity provision in event-contract markets shares structural similarities with underwriting rather than traditional inventory-neutral intermediation.

I guess my point would be that neither sports bookmaking nor stock prop trading is entirely “traditional inventory-neutral intermediation”; Jane Street does not just earn a bid/ask spread on all of its trades. From his findings: Across the full NFL season: Passive liquidity providers accumulated net exposure in the direction of realized outcomes in the majority of markets In most cases, they had a terminal asset on one outcome and a terminal liability on the other Aggregate profitability was positive (approximately $29 million) On average, the sum of terminal assets was greater than the sum of terminal liabilities Weekly P&L exhibited significant volatility, with pronounced drawdowns during adverse weeks LPs [liquidity providers] are winning on average, but are not without weeks of significant losses Yeah I mean seems fine? The job is to make markets where you have a positive expectation, and to win more than you lose. Elsewhere: Right, see, that’s (one-sided) model-based positive-expected-value [6] passive liquidity provision. Prediction market resolution | In general, event contracts on prediction markets pay $1 if an event happens and $0 if it doesn’t. But how do you know, in general, if an event has happened? Or rather, how does the prediction market know: How does it decide whether to pay out the Yes contracts or the No contracts? There are some events that have official results. Major League Baseball has a mechanism for deciding the winner of the Mets game, and a sportsbook or prediction market will probably defer to the official mechanism. The Oscars have official results. US elections, so far, have had official results. But most events in the world do not have official results. There is no official objective arbiter of whether US ground troops have entered Iran. The people who might know — the US military, the Iranian military — might not want to tell you. Or — as we discussed last week — you might know all the facts, but still not be sure whether those facts mean that “US ground troops have entered Iran” in the relevant sense. So who decides, and how? The most straightforward answer would be something like: - The prediction market is a regulated financial exchange with a lot of lawyers.

- The prediction market appoints a committee of lawyers and philosophers to decide whether events have occurred. [7]

- They try to do a good job.

- If they do a bad job, the prediction market loses customers, or regulators step in.

- The committee evolves a code of ethics: Committee members aren’t allowed to trade themselves, or take bribes, etc.

- The committee evolves a set of rules to make the substantive decisions. Each time some event contract has a difficult and controversial determination, the committee changes the rules for future event contracts to make the resolution easier and less controversial. If the “Cardi B performs at the Super Bowl” contract settles ambiguously because Cardi B danced and mouthed words but might not have been singing, you write future “_____ performs at _____” contracts to avoid that ambiguity. You do this over and over again, incrementally fixing rough patches, so that, in 10 years, prediction markets resolve as consistently and unsurprisingly as, you know, credit-default swaps or bank contingent capital securities. Which is to say: not perfectly consistently or unsurprisingly. But hopefully good enough for institutional use.

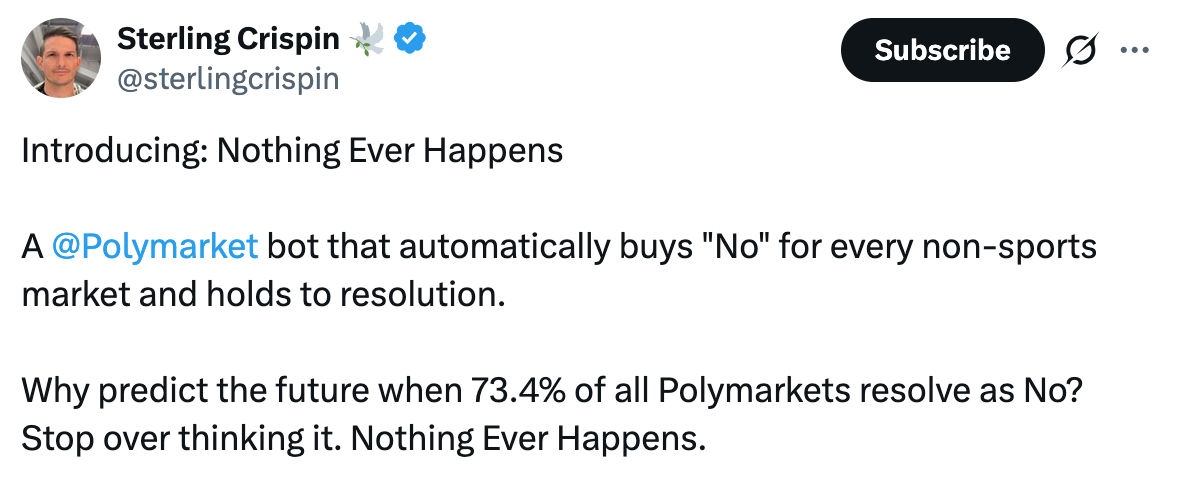

I think that, at a high level, this is roughly the approach of Kalshi, one of the two big prediction markets and the one that leans most into being a regulated US commodities futures exchange. I mean, we are in very early innings. I don’t think there’s necessarily a committee of philosophers and lawyers yet. But there are both regulatory and commercial pressures to get this stuff more or less right. Meanwhile Polymarket, the other big prediction market, started out crypto-y, so it takes a crypto-y approach to resolving events. Crypto things love to be decentralized and do stuff with tokens, and Polymarket’s resolution mechanism is decentralized and tokenized. As the Wall Street Journal describes it: Polymarket doesn’t resolve disputes itself. Instead, it relies on a service called UMA that runs a crowdsourced, crypto-based arbitration process for prediction markets. When a dispute arises, holders of UMA’s digital tokens debate the situation in forums on the social-media platform Discord, then vote on the outcome. UMA “governs this process to ensure fairness and transparency,” Polymarket says on its website. Still, UMA has been a lightning rod for controversy in previous resolution disputes. Some traders have complained that the process is ripe for manipulation by anonymous UMA “whales” whose holdings of the token gives them outsize voting power. And the Guardian notes: Different individuals hold different amounts of UMA, and therefore have different voting power. It isn’t known who the largest UMA holders are, or what might affect how they vote. It is entirely possible that the people who finally settle a bet on UMA have large amounts of money staked on it. “It’s the protocol that you should vote the right way,” said Ben Yorke, formerly a researcher at Cointelegraph. “But [UMA] gets it wrong all the time. And there have been cases where votes are decided by, like, one or two very large UMA holders.” And here is a Substack post on “How To Rig a Disputed Election’s Prediction Markets for $10 Million or Less,” arguing that you could manipulate Polymarket resolutions by buying up some UMA tokens, or manipulate Kalshi resolutions by bribing Kalshi. I suppose the Polymarket approach is a little bit like the resolution mechanism for credit default swaps, which does involve a vote of a committee of big CDS traders. But Polymarket’s is considerably more crypto-y. We keep talking about this: about whether US ground troops entered Iran, whether Cardi B performed at the Super Bowl, whether Iranian missiles landed in Israel, whether Ali Khamenei “left office” as Supreme Leader of Iran. There keep being disputes and ambiguities and confusion. Why? I think there are two possibilities: - Because prediction markets are just little babies, in some practical sense barely one year old; they are learning on the job and there are lots of problems to be worked out. Check back in in 10 years and everything will run as smoothly as any other financial market. (Which, again, is not perfectly smoothly!)

- Because prediction markets are fundamentally different from other financial markets. Other financial markets pay $X if the trading price of Y is above $Z; the range of possibilities is narrow and susceptible to objective measurement. Prediction markets pay $1 if any possible event in the world occurs, and there will always be new sorts of events and new complications. The philosophers will stay busy, and in 10 years there will be currently unimaginable ambiguities still making resolutions controversial. “How can you say the aliens have landed when in fact they hover,” people will object in the comments, but the committee has to make a decision.

Okay I’ve got a business model for Dario Amodei. Here’s what you do. You build an incredibly powerful artificial intelligence system that “is capable of identifying and then exploiting vulnerabilities in every major operating system and web browser when directed by a user to do so.” Then you hack into all the banks and steal all of their money. “It may be difficult to know what role money will play in a post-artificial general intelligence world,” you cackle, surrounded by bags of loot with dollar signs on them. Obviously this is not legal advice and there are flaws in this business plan, though you shouldn’t overstate them. (When the police come to arrest you, you hack into their computers too and send them to the wrong address, etc.) It turns out that, so far, “artificial intelligence” seems to be better at computer programming than at most other domains of human intelligence. But being really good at computer programming is, in our modern world, pretty useful. Anyway Bloomberg News reported last week: Treasury Secretary Scott Bessent and Federal Reserve Chair Jerome Powell summoned Wall Street leaders to an urgent meeting on concerns that the latest artificial intelligence model from Anthropic PBC will usher in an era of greater cyber risk. … Anthropic’s Mythos is a more powerful system that the AI firm has said is capable of identifying and then exploiting vulnerabilities in every major operating system and web browser when directed by a user to do so. Regulators’ caution about the power of the model in hackers’ hands echoes Anthropic’s own prudence. Anthropic has limited the release of it to just a few major technology and finance firms at first. Those companies, which include Amazon.com Inc. and Apple Inc. as well as JPMorgan Chase & Co., are part of “Project Glasswing,” which will work to secure the most important systems before other similar AI models become available. Right right fine in the actual world Anthropic is working with the banks to secure their systems against other similar models, because its actual business model is mostly being an enterprise AI company. But, you know, on a blank slate you might say “well if we could send ourselves all the money that would be good.” I feel like the simple model is: - What young people want, in a stock brokerage or any other service, is a well-designed app on their phone that allows them to get things done without ever talking to a human.

- What old people want, in a stock brokerage or any other service, is a person they can talk to directly to get things done without ever messing around with an app.

I say this as someone who was once young and is now old. A lot of people are in my situation, though; it is in the nature of humanity that we start young and become old. If you are a brokerage, or any other service provider, you gotta keep up. Bloomberg’s Charlie Wells and Paulina Cachero report: Robinhood, eToro, Revolut and Public.com are often associated with twentysomethings in their parents’ basements. Now those brokerage firms are offering investors access to airport lounges, gala dinners and Formula One races. They’re rolling out $695 premium credit-cards made of precious metals, creating elite concierge services exclusively for customers with million-dollar balances and pushing into complex tax planning, wealth management and even trust accounts in a bid to compete with more established rivals. … Revolut, a London-based fintech company, has been making strides into private banking and is planning more products targeting high-balance consumers. Revolut has also sought to hire multi-lingual private bankers to on-board high-net-worth individuals, cross-sell and give financial advice. The pitch from Public’s chief operating officer, Stephen Sikes, is that better data, content and AI tools are making people more comfortable managing even tens of millions of dollars themselves. His firm has hired concierges to talk trading with high-value customers, build rapport with potential members and improve their experience. Right sure you’re comfortable managing tens of millions of dollars yourself, but if you call your broker you want someone to answer. The basic push/pull with artificial intelligence and white-collar jobs is that, if you can get an AI to do 90% of your job, you will be more productive and have more leisure time, but if your boss notices, you might get fired and replaced by the AI. There are various, like, online quizzes to help you figure out of you are more likely to benefit from this dynamic or get fired, but one simple heuristic is: If you are the chief executive officer and controlling shareholder of a trillion-dollar company, you’re probably safe. Go ahead and automate yourself. No one is going to fire you, because nobody can fire you. The Financial Times reports: Meta is building an artificial intelligence version of Mark Zuckerberg that can engage with employees in his stead, as part of a broader push to remake the Big Tech company around AI. The $1.6tn group has been working on developing photorealistic, AI-powered 3D characters that users can interact with in real time, according to four people familiar with the matter. The company recently began prioritising a Zuckerberg AI character, three of the people said. The Meta chief is personally involved in training and testing his animated AI, which could offer conversation and feedback to employees, according to one person. They added that the character was being trained on the billionaire’s mannerisms, tone and publicly available statements, as well as his own recent thinking on company strategies, so that employees might feel more connected to the founder through interactions with it. I hope he will have his robot 1-on-1s in the metaverse, ha ha ha ha ha, remember the metaverse? I do think that “feel more personally connected to Mark Zuckerberg by interacting with an animated AI clone of him” is really the culmination of everything Facebook/Meta has worked for since its founding. In the future, most of everyone’s friends will be AI Mark Zuckerberg. Ackman Starts Marketing Pershing IPO to Raise up to $10 Billion. Goldman Shares Fall as Bond Trading Miss Outweighs Equity Record. Commodity traders lost ‘billions’ in early days of Iran war. Wrong-Way Bets on Oil Had a Star Trader Hundreds of Millions in the Hole. Energy Trader Vitol Reorganizes Derivatives Team After Losses. SpaceX Deal Lines Up $3 Billion in Tax Savings for EchoStar CEO. America’s New Tax Mantra: ‘The IRS Isn’t Going to Catch Me.’ Hollywood Heavyweights Sign Letter Opposing Paramount’s Deal for Warner Bros. Perella Weinberg to buy London advisory boutique Gleacher Shacklock. Surge in Hedge Fund Money Transforms an Old Insurance Market. BISTRO, CDO, SRT. Anxious Parents Are Spending Upwards of $50,000 to Land Their Kid a Job. Molotov cocktail thrown at home of OpenAI chief executive Sam Altman. When Bill Ackman Vented Over $2 Million, Fellow Billionaires Rushed to Commiserate. After Criticizing Pope, Trump Posts Image of Himself as a Jesus-Like Figure. If you'd like to get Money Stuff in handy email form, right in your inbox, please subscribe at this link. Or you can subscribe to Money Stuff and other great Bloomberg newsletters here. Thanks! |