|

I had a much more elaborate piece ready on the convergence between physical and futures markets… but given recent events, we’ll keep this to a quick take. It’s all still very fresh, with plenty of details to be clarified, yet the market is already treating this as the capitulation of the whole saga.

|

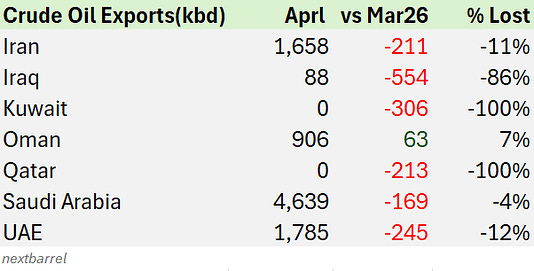

First, let’s look at where we’re coming from. If we thought March couldn’t get any worse in terms of export volumes out of the Middle East, April is now feeling the impact of the shut-ins. (Export volumes here mean cargoes loaded, whether they actually transit the strait or not.)

|

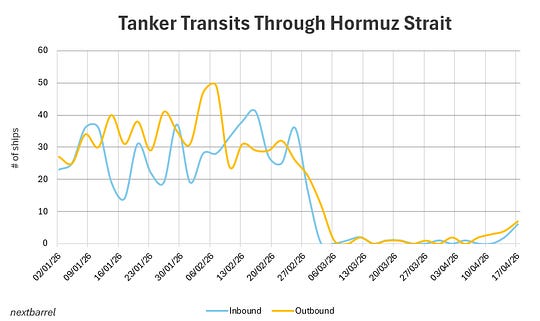

These figures will depend on how many ships they can secure over the next… six days? The strait is supposedly open during the ceasefire, which expires next Thursday. That doesn’t give much certainty when deciding whether to enter the Persian Gulf, given that the turnaround time for a tanker going in and out of the strait is at least five days.

Within hours of the announcement, there were some attempts to cross, in fact, we’ve already seen a few transits in both directions this week, although still far from historical averages.

|

We’ll need time to see how many vessels actually transit over a given period to gauge how “open” the strait really is. That said, we should expect a surge of crossings in the coming hours, this window of confusion may be the best opportunity, since no one knows how long it will last. No one expects attacks on merchant shipping in the coming days, nor tolls or enforcement of a U.S. blockade. The only real question is whether there are mines or not.

But let’s assume this is over, and vessels can move freely, what should we expect?

|

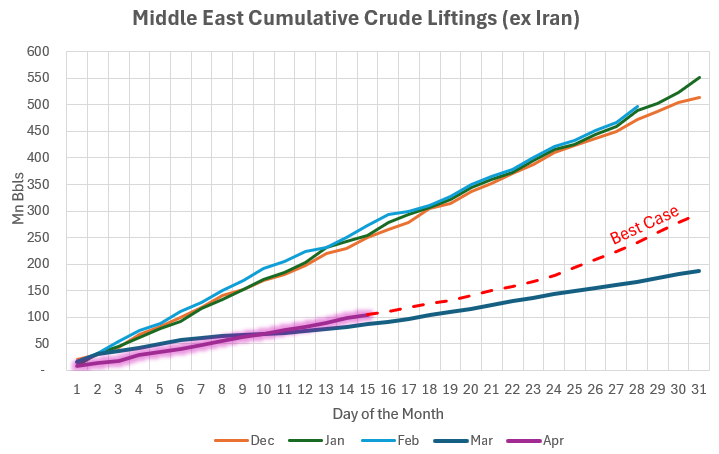

Even though we still lack clear signals on restoring production (that’s more of a three-month view), there are over 70 million barrels sitting in onshore storage, ready to be loaded. That alone could drive a near-term uptick in volumes, but even then, half of April is already lost. At best, we might load an additional ~3 Mbpd versus March, still far from normalization.

What we will see, beyond a collapse in flat price, is a reset in FOB differentials. Not only do we have incremental barrels from terminals, but also all the barrels that would suddenly be released from the Persian Gulf. Those 150–170 million barrels hit the very front of the curve, and they exceed what the system can process in the short term. Working through that will take weeks, depending on vessel flow.

What could shift as a result is the balance of power between charterers and shipowners. Until yesterday, they were still negotiating who would bear the risk of delays, and how to define “laycans” (the time window for a vessel to arrive at the terminal).

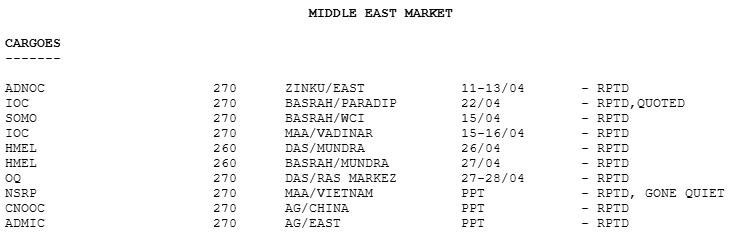

After the announcement, there were rumors of a fixture at WS650, but nothing confirmed. What did change is that shipbrokers’ phones started ringing again with cargo offers. Prior to the announcement, there were only a handful of stems available.

|

Setting logistics aside, can we infer anything from price action in the region?

|

The announcement came after the Dubai market close, but this benchmark hasn’t been giving meaningful signals for weeks. Ever since the April swap started trading, it’s effectively been dead. At this point, OSPs and allocations matter far more than anything coming out of financial markets.

We might, however, infer something from what we saw today in futures. Today’s drop, combined with the steady compression in spreads throughout the week, points to saturation across the entire energy trade. It was particularly evident in gasoil, where the concentration of longs did the most damage. On the other hand, equities rebounded much faster than expected, suggesting that the tourists are heading for the exits.

The one positive, if any, is that we’ve likely found a floor. The market is now pricing in a fast and definitive resolution. From here, the asymmetry in risk is to the upside...

Keep reading with a 7-day free trial

Subscribe to Oil not dead to keep reading this post and get 7 days of free access to the full post archives.

A subscription gets you:

| Oil Weekly Commentary | |

| A custom App and chat | |

| We might start doing webinars |

![]()

![]()