|

We are bouncing between $100 and $110, in a tense calm, where we have the feeling that something might shift beneath our feet anytime soon. The usual headline was followed by an ever decreasing reaction, but below the surface… below the surf… not going to lie.. nothing is going on, but I have some random thoughts:

|

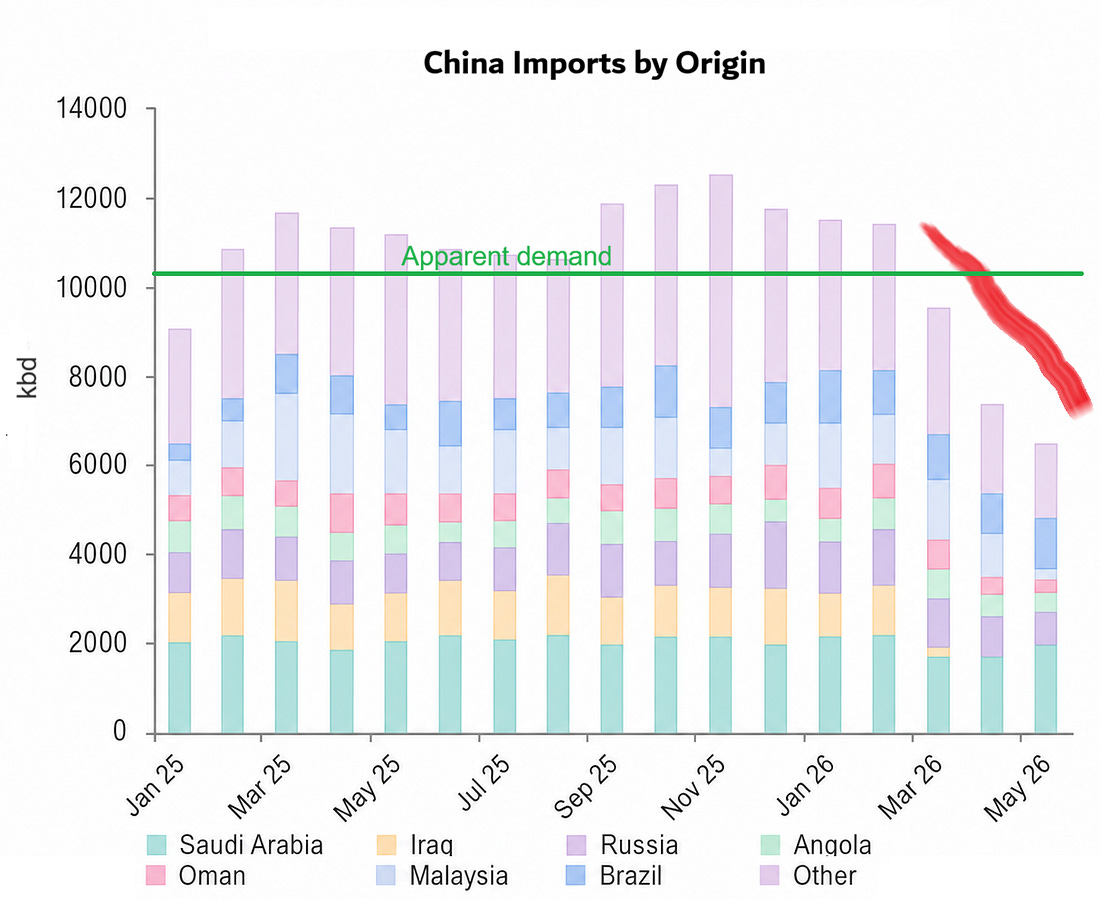

We have been lied to: Another month without transit through the Strait, another month where Chinese imports collapse. This is not sustainable anymore, not even with SPRs. Domestic product consumption in China has to be much lower than apparent demand, refining runs minus product exports plus product imports. If we assume average throughput of 14.5Mnbpd, subtract 600kbd of exports and add 50kbd of imports, the result is that China is supposedly burning around 13.8 to 13.9Mnbpd. The real number has to be much closer to the current 12.5Mnbpd they are actually refining. Sure, with the April product export ban they may have saved 400kbd, but that did nothing to alter the domestic dynamic. Wholesale gasoline and diesel prices are around $145/bbl, yet refining margins remain negative, consumption keeps falling week after week despite better prices and gas stations actively trying to stimulate demand.

If we lower the threshold for apparent demand, and if we take into account that China is producing 4.6Mnbpd domestically, then we can start imagining a future where imports are closer to 10Mnbpd than 12Mnbpd. This is probably an opportunity for them to normalize the numbers without openly showing weakness in the economy, because a 10% drop cannot be explained by prices alone.

|

Buying the Dip. There were a few early signs of China returning to the market for August barrels. One thing that broke the monotony of recent weeks was a handful of fixtures from WAF, some Dubai activity from Unipec, CNOCC cargoes not being offered to the open public, and more intra regional Southeast Asian cargoes appearing on the spot market, entailing some degree of normalization. There is a gap that China may be able to exploit, its Asian neighbors have already bought everything they need through August. June and July programs still look fairly deserted in terms of sales, freight rates are finally coming down and FOB differentials are no longer prohibitive, everything is lining up for China to come back and buy.

And it is not only China. Lately I have been hearing about traders buying back cargoes they sold early in March and April for loading during May, June and even July, many of those barrels were sold at Dated +10 or +15, and now they are trying to buy them back much cheaper. CNOOC and PetroChina sold a lot during those days, but also some Western IOCs (Shell, XOM) they are all now trying to close the short.

Assuming nothing changes, this is probably one of the last opportunities we will have to load physical crude at these kinds of differentials. We are not going to see anything like the panic buying from two months ago again, but we are probably not going to stay at these miserable +2 levels either.

Credit Freeze. There is another conversation emerging in the background that may be holding the market back. Financing physical cargoes is becoming difficult. It was already hard to secure a $60M letter of credit for 60 days, now that same cargo is worth $120M and interest rates are exploding higher. On top of that, some importers are struggling to source dollars and fears of defaults are growing. There is a Russian diesel cargo that has been waiting two months to discharge in Chile for a Bolivian distributor. Kenya, Ghana, Sri Lanka, nobody wants to sell them a cargo anymore. This is especially affecting asset light traders, who are sticking to safer trades, transatlantic arbs or supplying their own refineries. The rest of these high risk operations are increasingly being handled by opaque traders with some kind of state backing. today a cargo has at least $1/bbl embedded in financing costs.

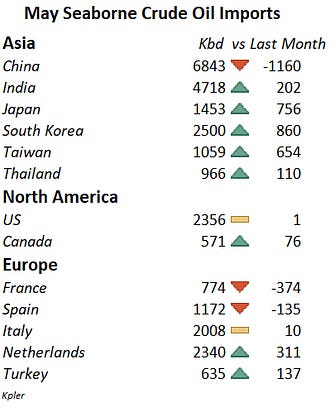

You can call it marginal demand destruction, but it is definitely redirecting cargoes toward the best paying customers, Korea, Japan, Europe.

Freedom of the Seas. There is a subtle shift in sentiment within the maritime world regarding Hormuz. The shipping community is realistic and is beginning to accept that it may have to live with this for a while longer. That is why we are already seeing shipowners willing to take more risks, Eastern Med, Dynacom and others, and this week the main government shipping bodies issued guidance that was basically Crossing the Strait for Dummies. Indirectly, I think they are saying that nobody is coming to save them, neither through a deal reopening the Strait nor by bombing the hell out of Iran. There is evidence of some kind of underground arrangement, where certain ships are entering and leaving without issues. Just look at the Karolos, already on its way to a second Iraqi cargo in a week.

This exhaustion is also becoming visible in freight rates, which have started falling even for ex Yanbu and Fujairah cargoes. Shipowners are noticing increased risk aversion from the Chinese side, and some trader relets have managed to get out. There is also growing pressure from seafarer unions to ease the humanitarian situation for trapped crews, and until last week there was still the risk of attacks on Iran resuming, nobody wants to end up caught in the crossfire.

US Export Bans. Once again there are rumors circulating that the Trump administration, seeing no progress in negotiations while entering peak gasoline demand season, could introduce some kind of restriction on refined product exports as a last resort. Personally I do not believe it, but I also do not think draining gasoline inventories at this pace is sustainable for much longer. The middle ground solution would be temporary export quotas, restrictions on certain octane grades, or suspending some environmental blending obligations for a while in order to lower retail prices. It sounds absurd today, but if they do nothing different, driving season starts with gasoline at $5 per gallon...

Subscribe to Oil not dead to unlock the rest.

Become a paying subscriber of Oil not dead to get access to this post and other subscriber-only content.

A subscription gets you:

| Oil Weekly Commentary | |

| A custom App and chat | |

| We might start doing webinars |

![]()

![]()